In an internal webcast hours after the shared-workspace provider delayed its stock-market listing, Neumann said he had lessons to learn about running a public company, according to the Financial Times. He also voiced regret over how the listing process was handled, the newspaper said, citing people who saw the presentation.

Neumann's larger-than-life personality played a "huge role" in the listing's failure, the Financial Times reported, citing someone who worked closely with him. Fears of emulating the disappointing public debuts of Uber, Lyft, and other disruptive businesses this year factored into Neumann's decision to postpone WeWork's IPO, people close to the cofounder told the newspaper.

Neumann and two other WeWork executives vowed to employees the IPO would go through later this year, but the company could be forced to delay its public debut until next year, people briefed on the matter told the Financial Times. WeWork was expected to drum up interest in its shares during an investor roadshow this week, before listing them on the Nasdaq index next week.

Investors grew disillusioned with WeWork's unclear path to profitability, business model, complex structure, hefty valuation, and controversial governance. The group slashed its targeted public valuation to below $20 billion — less than half the $47 billion private valuation it secured in January — and introduced new limits on Neumann's control of the company, stock sales, real-estate deals, and succession plans, but failed to win enough support.

WeWork hopes a fresh set of quarterly financials for the three months to September will help it to revive its IPO next month, according to Reuters, citing people familiar with the company's thinking. However, investor demand could prove lackluster as fund managers become more conservative and look to protect their gains in the fourth quarter, Reuters said.

WeWork must raise at least $3 billion through an IPO this year, or it will lose out on a $6 billion credit line tied to that milestone, forcing it to seek alternative financing.

President Donald Trump has called Federal Reserve Chairman Jerome Powell 'clueless.' | Drew Angerer/Getty Images

President Donald Trump has taken over Jerome Powell’s life.

The Federal Reserve’s expected decision on Wednesday to cut interest rates again will spark new questions about whether Powell, its chairman, is caving to intense public pressure by Trump. While Powell strongly rejects that notion, the president’s policies have clearly forced the central bank’s hand.

Story Continued Below

The Fed, which last December was considering hiking interest rates at least twice this year, has done a head-spinning turn since then in response to weakening business investment, a contraction in manufacturing and a global slowdown — all fueled by Trump’s trade wars.

And the president’s abrupt decision last year to pull out of the Iran nuclear accord arguably set off a steady deterioration in relations that today has made Middle East tensions another threat to economic growth that the Fed must take into account.

Trump is forcing still more dramatic policy options into the limelight — including his latest call on the Fed to cut rates below zero, an idea that the central bank has long resisted as an avenue for fighting recessions.

“I’ve always thought the Fed has been a little bit slow to control the narrative about monetary policy,” said Seth Carpenter, chief U.S. economist at Swiss bank UBS and a former Fed official. “Throw Trump into the mix, and you’re in a completely different circumstance where he does like to drive the narrative.

“You just end up being dragged around,” he said.

The Fed has repeatedly pointed to trade tensions, slowing global growth and muted inflation as its main reasons for lowering rates, a move intended to support the economy as recession fears have begun to creep into the Treasury bond market.

But the economy is still growing, with consumer spending powering it forward and the labor market continuing to add jobs, suggesting some room for optimism about the future of the expansion, the longest in U.S. history.

The Fed has remained reticent to share details about its plans as it closely monitors the complicated economic picture. After the central bank lowered rates in July — its first cut in more than a decade — Powell suggested that the Fed wasn’t yet embarking on a full-blown cutting cycle. But markets are expecting several more reductions between now and early next year and will be watching the chairman closely for signals on that front.

But those decisions will be driven, at least in part, by the outcome of the U.S.-China trade war, meaning the Fed, like the rest of Washington, will continue to keep an eye on Trump’s Twitter storms.

Against that backdrop, Trump tweets, often daily, that the Fed is clueless and that if it would only slash rates by a large amount, the economy would take off like a “rocket ship.”

“The United States, because of the Federal Reserve, is paying a MUCH higher Interest Rate than other competing countries,” the president tweeted on Monday. “They can’t believe how lucky they are that Jay Powell & the Fed don’t have a clue,” he added, calling for a “Big Interest Rate Drop.”

His recent attempt to push the Fed to pursue negative interest rates — a move tried in Europe and Japan with unclear results — demonstrates the shift in who is controlling the narrative around the Fed.

A decade ago, the central bank pursued a range of new and untested policies to jump-start the economy — such as purchasing trillions of dollars in government bonds — and faced challenges in getting the public on board. Now, while the pursuit of negative rates in the U.S. would still be highly controversial, Trump is the one driving the conversation toward unconventional policies.

“There’s no escaping the president’s bully pulpit, no matter what it is he’s talking about, not the least when it comes in the form of a tweet where it gets promoted and dissected,” said Sarah Binder, a political science professor at George Washington University. “It focuses media attention. It focuses public attention.”

Trump has also urged the Fed to help him more directly fight his trade wars, focusing much of his frustration on the heft of the dollar, whose strength makes U.S. exports more expensive.

He has gone from suggesting the central bank cut its main borrowing rate by a whole percentage point — the equivalent of four standard cuts — to now calling for rates of “ZERO, or less,” which would mean lowering rates by at least 2 percentage points.

“He certainly is the big elephant in the room,” Binder said.

“If part of [Fed] communications is telling markets and the public and businesses where you’re headed, and if people wonder where they’re headed because the president has now injected himself into the debate … then that kind of undermines the whole use of communications as the central tool” of monetary policy, she added.

As for the Fed’s ultimate decisions on rates, Carpenter said he believes central bank officials when they insist that they do not discuss the political implications of their decisions at their policy meetings. But, he said, the pressure likely makes them more cautious.

“Their lives are just made that much more complicated by having to second-guess themselves, and saying, ‘OK, now we’ve made a decision, let’s ask ourselves one more time, are we sure we’re doing this for the right reasons?‘”

Americans with credit card debt won’t get much help from the Federal Reserve's interest rate cuts.

Continue Reading Below

The Fed is slated to cut its benchmark interest rate by a quarter-percentage point to a range of 1.75 percent to 2 percent following its two-day meeting on Wednesday – but it won’t be shaving much off credit card bills, experts say.

“Relief credit card holders get from the Fed won’t be huge. It’s not something that’s going to move the needle for most folks with just this one rate reduction,” Matt Schulz, chief industry analyst at Comparecards.com, told FOX Business. “In terms of reduction on your actual monthly bill, you’re only talking about a few dollars a month for most people.”

The average household credit card debt is $5,700, according to the Fed. The last rate cut dropped the minimum payment by just $1 per month. So minimum payments towards a $5,700 debt at 17.61 percent would keep someone in debt for 19 ½ years racking up $7,415 in interest.

MORE FROM FOX BUSINESS.COM...

Here's what you can do now to help manage credit card debt:

Advertisement

Consider a balance transfer card

Balance transfer cards allow users to take a high-interest debt from one or more credit cards and move it to another card with a lower interest rate. This means card holders can apply more payments to the principal balance every month, rather than racking up interest charges, which can help some reduce credit card debt faster.

“It can seem counterintuitive to take on credit card debt by getting another credit card, but if you use those zero percent balance transfer cards it can save a ton on interest. You’re talking about going a year and half without interest,” Schulz advised.

Fed rate cuts won't give Americans in credit card debt much relief, experts say.

Cards like Chase Slate, American Express Everyday or BankAmericard offer 15 months with no interest and no transfer fee.

Still, some experts fear that more interest rate cuts could lead credit card issuers to be less generous with zero percent interest periods, or implement higher transfer fees.

“Right now, 87 percent of balance transfer cards charge a transfer fee typically between 3 percent to 5 percent. Falling rates could also spur issuers to raise other fees such as foreign transaction fees and annual fees,” Ted Rossman, an industry analyst, said.

Lower your Annual Percentage Rate

The average credit card annual percentage rate is between 17 and 24 percent, and industry experts suggest asking your credit card company to reduce their APR.

“People have more power over the credit card issuer than they realize, but way too few people actually wield it. If you have good credit, a good track record and you’re willing to pick up the phone, there’s a good chance you can get your APR reduced to a greater degree,” Schulz said.

There's also the option to negotiate payment terms, and ask for a smaller minimum payment. Those who are longtime customers making payments on time will have a better standing when negotiating.

And consdering the average American has a credit score of 704, according to FICO, the highest in the history of credit scoring, most may be more likely to qualify for a lower interest rate.

Automate payments

Automating payments is a simple way to ensure you're making payments on time to avoide racking up late fee costs and maintaing a good credit score. Paying more than the minimum is recommended, since banks make money off interest charged each pay period.

(Reuters) - As if the U.S. Federal Reserve didn’t already have enough on its plate heading into its meeting on interest rates this week, chaos deep inside the plumbing of the U.S. financial system has thrown policymakers an unexpected curveball.

FILE PHOTO: Federal Reserve Board building on Constitution Avenue is pictured in Washington, U.S., March 19, 2019. REUTERS/Leah Millis/File Photo

Cash available to banks for their short-term funding needs all but dried up on Monday and Tuesday, and interest rates in U.S. money markets shot up to as high as 10% for some overnight loans, more than four times the Fed’s rate.

That forced the Fed to make an emergency injection of more than $50 billion, its first since the financial crisis more than a decade ago, to prevent borrowing costs from spiraling even higher. It will conduct another one on Wednesday.

The exact cause of the squeeze is a matter of some debate, but most market participants agree that two coincidental events on Monday were at least partly to blame. First, corporations had to withdraw funds from money market accounts to pay for quarterly tax bills, and then on the same day the banks and investors who bought the $78 billion of U.S. Treasury notes and bonds sold by Uncle Sam last week had to settle up.

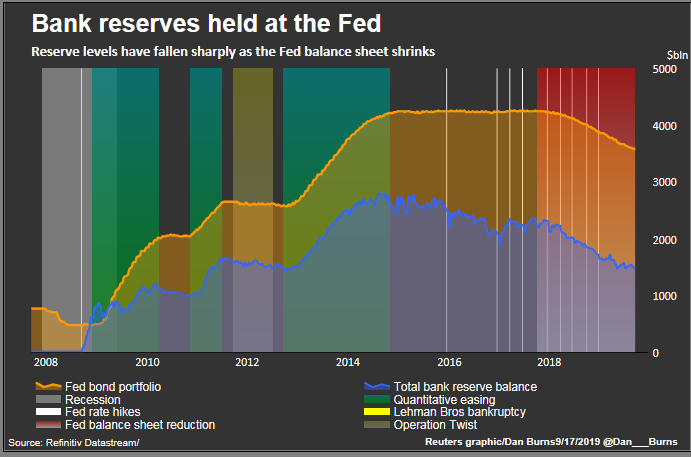

On top of that, the reserves that banks park with the Fed and are often made available to other banks on an overnight basis are at their lowest since 2011 thanks to the central bank’s culling of its vast portfolio of bonds over the past few years.

Added together, these factors are testing the limits of the $2.2 trillion repurchase agreement - or repo - market, a gray but essential component of the U.S. financial system.

Whatever the cause, the episode has added fuel to the argument that the Fed needs to take steps to avoid more disruptions in the repo market down the road.

The repo market underpins much of the U.S. financial system, helping to ensure banks have the liquidity to meet their daily operational needs and maintain sufficient reserves.

In a repo trade, Wall Street firms and banks offer U.S. Treasuries and other high-quality securities as collateral to raise cash, often overnight, to finance their trading and lending activities. The next day, borrowers repay their loans plus what is typically a nominal rate of interest and get their bonds back. In other words, they repurchase, or repo, the bonds.

The system typically hums along with the interest rate charged on repo deals hovering close to the Fed’s benchmark overnight rate, currently set in a range of 2.00% to 2.25%. That rate is expected to be cut by a quarter percentage point on Wednesday.

But sometimes, investors get fearful of lending, as seen during the global credit crisis, or at other times there are just not enough reserves or cash in the system to lend out, as appeared to be the case this week. And that can cause a squeeze on the market and send borrowing costs zooming higher.

But when investors get fearful of lending, as seen during the global credit crisis, or when there are just not enough reserves or cash in the system to lend out, it sends the repo rate soaring above the Fed Funds rate.

Trading in stocks and bonds can become difficult. It can also pinch lending to businesses and consumers and, if the disruption is prolonged, it can become a drag on a U.S. economy that relies heavily on the flow of credit.

WHAT HAS CAUSED THE DROP IN BANK RESERVES?

Coming out of the financial crisis, after the Fed cut interest rates to near zero and bought more than $3.5 trillion of bonds, banks built up massive reserves held at the Fed.

But that level of bank reserves, which peaked at nearly $2.8 trillion, began falling when the Fed started raising interest rates in late 2015. They fell even faster when the Fed started to cut the size of its bond portfolio about two years later.

The Fed stopped raising interest rates last year and cut them in July and is expected to do so again on Wednesday. It has also now ceased allowing to bonds to roll off its balance sheet.

The question vexing policymakers now is whether those actions are enough to stop the downward drift in reserves, which are a main source of liquidity in funding markets like repo.

Bank reserves at the Fed last stood at $1.47 trillion, the lowest level since 2011 and nearly 50% below their peak from five years ago.

Through the Federal Reserve Bank of New York, the Fed can conduct occasional spot repo operations at times of funding stress, allowing banks and dealers to swap their Treasuries and other high-quality securities for cash at a minimal interest rate. It did this on Tuesday and will do it again on Wednesday.

2. LOWER THE INTEREST IT PAYS ON EXCESS RESERVES

By making it less profitable for banks, especially foreign ones, to leave their reserves at the Fed, it may encourage banks to lend to each other in money markets.

3. CREATE A STANDING REPO FACILITY

Such a permanent financing program will allow eligible participants to exchange their bonds for cash at a set interest rate.

Fed and its staff have considered such a facility, but they have not determined who qualifies, what would be the level of interest paid and the timing for a possible launch.

4. RAMP UP BUYING OF TREASURIES

The Fed can replenish the level of bank reserves by slightly increasing its holdings of U.S. government debt. This comes with the risk that it may be perceived as a resurrection of quantitative easing rather than a technical adjustment.

Reporting by Richard Leong; Editing by Dan Burns and Richard Borsuk

Anheuser-Busch InBev NV is the world’s largest brewer. It is looking to list its Asian business on the Hong Kong stock exchange.

Photo:

Kyle Lam/Bloomberg News

The world’s largest brewer is taking a second shot at listing its Asian business, seeking to raise up to US$7.6 billion in Hong Kong, even as the city reels from a summer of protests and from trade tensions between the U.S. and China.

The regional unit of brewing behemoth

Anheuser-Busch InBev SA

BUD -0.68%

said on Tuesday it would begin taking orders the following day for its Hong Kong initial public offering, ahead of a planned listing on Sept. 30.

The unit, Budweiser Brewing Co. APAC, plans to raise a baseline 34 billion to 37.9 billion Hong Kong dollars (US$4.35 billion to US$4.84 billion) by selling new shares, at a market value of US$45.6 billion to US$50.7 billion. If demand is strong, AB InBev could boost the deal’s size to as much as US$7.6 billion.

Smaller, but Faster-Growing

How Anheuser-Busch InBev's new and old Asian businesses stack up, after the sale of its Australian operations.

In July, AB InBev shelved an earlier attempt to list the business, after seeking to raise nearly US$10 billion, at a valuation of up to US$63.7 billion. It said market conditions were partly to blame, but some prospective investors and analysts pointed to its high valuation aspirations.

It is now marketing a smaller, faster-growing business that is more focused on China and other emerging markets, after selling its Australian unit—which had been part of the original listing plan—to Japan’s

Asahi Group Holdings Ltd.

for US$11.3 billion.

“We are even more of a growth company than two months ago, when we were first here,” Budweiser APAC Chief Executive

Jan Craps

told a news conference. “We believe now is the right moment to do the IPO.”

The revised stock sale would be the world’s second-largest IPO this year, after ride-hailing giant

Uber Technologies

UBER 3.55%

’ US$8.1 billion market debut in New York, according to Dealogic.

Unlike the last attempt, this time Budweiser APAC has secured a US$1 billion pledge from Singaporean sovereign-wealth fund GIC Pte. Ltd. to act as a cornerstone investor. Many Hong Kong listings use cornerstones, who invest wherever the deal prices, to help entice other prospective buyers.

East Meets West

Budweiser APAC has sharpened its focus on China and other high-growth markets in what it calls 'Asia Pacific West,' after selling out of Australia.

Shares by geographical breakdown, 2018

West

East

SeptEMBER deal

July deal

Volume

85%

15

79

21

Revenue

76

24

61

39

Ebitda*

72

28

51

49

Note: East is primarily South Korea, Japan, New Zealand and previously Australia. West includes China, India and Vietnam. *Normalized Ebitda, excluding exceptional items

Source: the company

Vincent Wen, an investment manager at KCG Securities Asia, said the addition of a prominent cornerstone could help ensure this sale went more smoothly.

Social unrest, the U.S.-China trade dispute and slowing Chinese growth are threatening to tip Hong Kong’s economy into recession. Sometimes-violent protests have disrupted flights and road transport, denting the city’s image as a safe location and an international financial hub. The benchmark Hang Seng stock index fell in late July and August, but has since rebounded somewhat, leaving it basically flat for the three months to Monday’s close.

“We can’t deny it’s a volatile and challenging environment today, but we believe Hong Kong is still the best financial center in Asia for us to do the listing,” Mr. Craps said.

Many issuers are testing investors’ appetite in both the equity and bond markets in Hong Kong, such as China’s Shanghai Henlius Biotech Inc.

The Budweiser APAC deal’s price range equates to 33.8 to 37.5 times the earnings management estimates the business could make next year, according to a summary of terms seen by The Wall Street Journal.

That is broadly in line with Hong-Kong listed Chinese brewers China Resources Beer Holdings Co. and

Tsingtao Brewery Co.

They trade at nearly 40 and roughly 30 times forecast 2020 earnings, respectively, Refinitiv data shows, after sharp gains this year.

AB InBev brews one in four of the world’s beers, and owns hundreds of brands including Budweiser, Stella Artois and Corona. But the deal-making saddled the brewer with debts, which it now aims to shrink to about US$80 billion.

JP Morgan,Morgan Stanley,

Bank of America Merrill Lynch and CICC are joint global coordinators.

—Julie Steinberg and Jing Yang contributed to this article.

Private equity chief Stephen A. Schwarzman, the founder of $545 billion Blackstone Group (BX), seems more conservative these days as it gets later in the market cycle.

In an interview with Yahoo Finance, he acknowledged that the consumer, which makes up about 70% of the U.S. economy, continues to be strong. But he warned of weakness in manufacturing even as stock and bond prices sit near record highs.

"Usually when everything's doing records all the time, and there's a lot of geopolitical uncertainty, it's usually like a wake-up call," he said. "It's not red, but it's yellow. And it makes you be more conservative when you're investing. It makes you think more about downsides. It makes you want to buy higher-quality things because your chance of accidentally being lucky, which happens at the bottom of the cycle, is much lower."

He added that this is a time where the U.S. will likely still be growing somewhere around 2% or maybe a "tiny bit less."

In his new memoir "What It Takes," Schwarzman outlined his three "simple rules" for identifying market tops and bottoms.

First, market tops are "easy to recognize" because overconfident buyers are of the mindset that "this time is different" when it's usually not. Second, cheap debt is fueling acquisitions and investments, and leverage levels accelerate. Third is "the number of people you know who start getting rich" and the number of investors "claiming outperformance."

"Loose credit conditions and a rising tide can make it easy for individuals without any particular strategy or process to make money 'accidentally,'" he wrote. "But making money in strong markets can be short-lived. Smart investors perform well through a combination of self-discipline and sound risk assessment, even when market conditions reverse."

The Blackstone Group Chairman & CEO Stephen A. Schwarzman. (AP Photo/Richard Drew)

In his four decades on Wall Street, Schwarzman has lived through seven market downturns: 1973, 1975, 1982, 1987, 1990-1992, 2001, and 2008-2010.

He explained that spotting a market bottom can be difficult and trying to time it is usually a bad idea.

"Most public and private investors buy too early and underestimate the severity of recessions,” he wrote. “It's important not to act too quickly.”

His best advice is to invest when markets have recovered at least 10% from their lows.

"Asset values tend to increase as economies gain momentum. It's better to give up the first 10% to 15% of a market recovery to ensure that you are buying at the right time."

The Federal Reserve is widely expected to cut interest rates at the conclusion of its two-day meeting on Wednesday.

Continue Reading Below

A rate cut would be the Fed’s second in the same number of meetings as it looks to keep the longest economic expansion on record going into a 12th year.

“The Fed will likely cut 25bp at this week’s meeting and guide toward further rate reductions,” New York-based Bank of America Merrill Lynch economists wrote Monday. “The meeting should have a dovish tone. However, in our view, the big question is whether Chair Powell continues to characterize the easing cycle as a 'mid-cycle adjustment."

Recent economic data has softened a bit as the U.S.-China trade war has stretched into its second year. The U.S. economy grew at an annualized 2 percent rate in the second quarter, down from the previous quarter’s 3.1 percent print. U.S. manufacturing and employment data have also shown signs of slowing.

“The United States, because of the Federal Reserve, is paying a MUCH higher Interest Rate than other competing countries,” Trump tweeted Monday.

Advertisement

“They can’t believe how lucky they are that Jay Powell & the Fed don’t have a clue. And now, on top of it all, the Oil hit. Big Interest Rate Drop, Stimulus!”

Trump isn’t the only one calling for a big rate cut.

St. Louis Fed President James Bullard, who is a voting member, said earlier this month an outsized 50 basis point cut is needed to get ahead of market expectations and cushion the economy from the U.S.-China trade war.

Still, traders at the CME Group are pricing in a 65.8 percent chance the Fed cuts rates by 25 basis points on Wednesday, down from more than 90 percent just last week. They see a zero percent chance of a 50bp cut.

Even without a 50bp cut at Wednesday's meeting, the Fed is expected to lower rates further before the end of the year.

“Beyond the September meeting, we continue to expect the FOMC to deliver a third and final 25bp cut to 1.5-1.75 percent in October,” a Goldman Sachs economics research team wrote Friday.

“A 75bp total realignment of the policy rate appears to be roughly the ‘mid-cycle adjustment’ following the 1990s template that the Fed leadership has in mind, a moderate response to moderate concerns about growth risks and soft inflation.

AP Photo/Mark Lennihan

AP Photo/Mark Lennihan

{kind=link}

{kind=link}