Amazon revolutionized online shopping and quickly became one of the most ubiquitous and successful businesses in the world. This is in part owed to it always being on the forefront of reinvestment without pausing to actually earn money. To get ahead of its retail competitors, the company announced that it's working on bringing free one-day deliveries to its Prime members during its earnings calls on Thursday.

Currently, Amazon's annual subscription service qualifies you to free two-day shipping with most products, and only when you order items totaling more than $35 do you receive free one-day shipping. The upcoming faster delivery will come at no additional cost or conditions for paying Prime members, though.

The company says it's working hard with its logistics partners to achieve this faster delivery to an ever-growing number of places in the US. However, it states that it will take a significant amount of time until the service is fully deployed and that it will give us additional information about its efforts in this year's second quarter. What we know now is that the service will start rolling out in the US and will be available globally eventually.

The announcement comes shortly after Amazon's quarterly earnings calls, where it revealed that its retail income is slowing, which is not surprising since a business can only grow so big. To retain customers, the company has to give them more incentives to keep them loyal to its online shop. While Amazon could wish for even more growth in retail, that doesn't mean it's in any financial trouble – today most of the internet behemoth's income comes from its cloud storage business, Amazon Web Services (AWS).

The troubles affecting Europe’s automakers are on full display Friday, as both Mercedes parent Daimler (DE:) and France’s Renault (PA:) reported falling sales in the first quarter.

The sold 7% fewer vehicles in the first quarter than it did a year earlier, with declines in all three of its most important regions – China (3%), Europe (4%) and the U.S. (9%). Earnings before interest and tax slid 16% although, at 2.8 billion euros ($3.1 billion), they still beat consensus forecasts by nearly 10%.

Even though outgoing Chief Executive Dieter Zetsche reaffirmed the company’s full-year outlook, the company’s shares were still down 0.3% on the news. That was lagging the local index, which was broadly unchanged.

The benchmark index was also flat, losing 0.12 points – less than 0.1% to 390.02. The U.K. was down 0.2%.

Daimler is facing a steep rise in investment obligations as it migrates to electric vehicles, along with its German peers Volkswagen (DE:) and BMW (DE:). The three are all facing the prospect of fines from the European Commission for colluding to keep sub-optimal diesel engines on the road when they had better technology available to deploy.

Renault has problems of a slightly different nature, most obviously in the enormous distraction created by the criminal charges against its long-time CEO Carlos Ghosn. The Wall Street Journal is reporting Friday that the French company is preparing to propose a merger with Nissan, its Japanese partner, hoping to restore a relationship that has been badly strained by the Ghosn affair.

Renault's greater exposure to emerging markets such as Turkey and Argentina has hurt it in recent months, and like its European rivals it has had to abandon hopes of making money in Iran in the wake of President Donald Trump’s decision to tighten sanctions on the country.

Renault’s sales were down 5.6%, although it eked out a 2% gain in Europe, its most important market. As a result, its shares outperformed the local , rising 1.7%.

Europe’s other carmakers such as Volvo (OTC:) and Peugeot (PA:) have also reported weak first quarters.

Disclaimer:Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. All CFDs (stocks, indexes, futures) and Forex prices are not provided by exchanges but rather by market makers, and so prices may not be accurate and may differ from the actual market price, meaning prices are indicative and not appropriate for trading purposes. Therefore Fusion Media doesn`t bear any responsibility for any trading losses you might incur as a result of using this data.

Fusion Media or anyone involved with Fusion Media will not accept any liability for loss or damage as a result of reliance on the information including data, quotes, charts and buy/sell signals contained within this website. Please be fully informed regarding the risks and costs associated with trading the financial markets, it is one of the riskiest investment forms possible.

Uber is reportedly looking to sell shares between $44 to $50, aiming to raise $8 to $10 billion in the offering. This would value the company between $80 billion to $90 billion, Bloomberg reports.

Previous reports had pegged Uber’s valuation at around $120 billion. Still, that valuation is higher than its last valuation of $76 billion following a funding round.

It’s likely this decrease in valuation is influenced by Lyft’s performance on the public market. Since its debut on the NASDAQ, Lyft’s stock has suffered after skyrocketing nearly 10 percent on day one.

While Uber has yet to officially set the terms of its IPO, the company is reportedly expected to do so as early as tomorrow. Even if Uber seeks the low-end of the expected range, it would be more than three time’s the amount of Lyft’s $2.34 billion IPO. It would also make Uber’s IPO the largest one in the U.S. since Alibaba’s in 2014.

In 2018, Uber reported 2018 revenues of $11.27 billion, net income of $997 million and adjusted EBITDA losses of $1.85 billion. Uber, which filed for its IPO two weeks ago, is expected to list on the New York Stock Exchange in May.

Starbucks on Thursday reported earnings that outpaced analyst expectations and raised its outlook for the year, as customers spent more at its cafes in the U.S. and sales growth in China was stronger than expected.

Shares of the company were unchanged in extended trading.

"We are especially pleased with our comparable store sales growth in our two lead markets, the U.S. and China, where we are also continuing to drive strong new store development with industry-leading returns," CEO Kevin Johnson said in a statement.

Here's what the company reported compared with what Wall Street was expecting, based on a survey of analysts by Refinitiv:

Earnings per share: 60 cents, adjusted, vs. 56 cents expected

Revenue: $6.31 billion vs. $6.32 billion expected

Same-store sales: 3% vs. 2.9% expected

The coffee chain reported fiscal second-quarter net income of $663.2 million, or 53 cents per share, up from $660.1 million, or 47 cents per share, a year earlier.

Excluding the sale of its Tazo brand, costs related to its licensing deal with Nestle and other items, Starbucks earned 60 cents per share, topping the 56 cents per share expected by analysts surveyed by Refinitiv.

The company raised its full-year earnings forecast. It is now expects adjusted, or non-GAAP, earnings per share in the range of $2.75 to $2.79, up from a prior range of $2.68 to $2.73. Analysts were forecasting 2019 earnings of $2.71 per share.

Net salesrose 5% to $6.31 billion, missing expectations of $6.32 billion.

The company reported same-store sales growth of 3%, beating Wall Street's estimates of 2.9%. Starbucks attributed the growth to a 3% increase in average ticket.

"While much of the beverage comp sales growth was driven by ticket, close to half of the ticket growth was from beverage mix and match, demonstrating that our higher margin premium offerings resonated with customers and customers bought more beverages per transaction," CFO Pat Grismer told analysts on the conference call.

Starbucks released one of those pricier drinks last month, the Cloud Macchiato, with help from pop star Ariana Grande. Johnson called the drink's launch "the second most viral Starbucks campaign ever." The beverage is part of its wider drink innovation strategy: focus more on cold drinks and less on limited-time offerings and Frappucinos. The strategy is meant to build more brand affinity to keep customers coming back to Starbucks' coffee shops regularly.

The chain also saw the best afternoon performance in three years, due to the popularity of its cold drinks and improved in-store experience. In the U.S., sales at stores open at least a year grew by 4%.

The company even saw same-store sales growth of 3% in China, where the company is facing increased competition from Luckin Coffee and a slowing economy.

"This performance is especially noteworthy when you consider the intensity of competition from discounting in China, as well as our aggressive pace of new store development," Johnson said.

However, transactions at stores open at least a year fell 1% in the country, meaning that traffic was declining.

In just four months, Starbucks added delivery to 2,100 of its stores in China through its partnership with Alibaba. Johnson said that the average delivery time is under 20 minutes. The company is planning to launch mobile order and pay in the country by the end of fiscal 2019.

In the second quarter, Starbucks Rewards reached 8.3 million active Chinese members. Executives said on the conference call that loyalty program members represent over 50% of its transactions in China.

Starbucks' loyalty program grew to 16.8 million active members in the U.S., up 13% from last year. The Seattle-based company recently revamped the program, offering a wider range of redemption options for members. The changes also mean that customers have to spend more to earn a free drink.

Unlike the last time that it made major changes to its loyalty program back in 2016, Starbucks has largely avoided social media backlash. COO Roz Brewer said that the company has also not seen as many phone calls to its customer service hotline as expected.

During its second quarter, the company added 319 net new stores, bringing its total to 30,184 worldwide. A whopping 94% of its openings were outside of the U.S., including a Reserve Roastery in Japan.

And Starbucks has no plans to slow down store openings in the second half of 2019. The company plans to add 2,100 net new stores globally. Nearly 600 of those openings will be in China, as rival Luckin plans to open 2,500 this year in an attempt to overtake Starbucks as the largest coffee chain in the country. Rather than mimicking Starbucks' homey store concept, the fast-growing newcomer's strategy has focused on stores designed for convenience and easy pick-up.

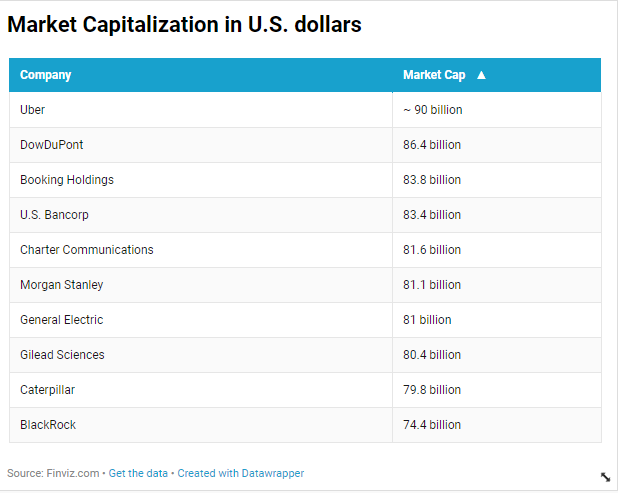

Uber could go public at a stock price that would make it bigger than some of the best-known names in the S&P 500.

The ride-hailing company plans to list shares between $44 and $50 in its upcoming initial public offering, several news outlets reported Thursday, citing people familiar with the matter. That would value the company at as high as $90 billion when it lists on the New York Stock Exchange, according to a Bloomberg report.

The eye-popping figure would make it more valuable than S&P juggernauts like DowDuPont, General Electric and Caterpillar, according to data from Finviz.com. It would also top Morgan Stanley and BlackRock, with market capitalizations of $81 billion and $74 billion, respectively.

Market capitalization, or "market cap," is the total dollar amount of a company's outstanding shares, which can be calculated by multiplying the firm's outstanding shares by the price of one share.

Uber is different from its potential market-cap peers in a key way — it's not making money.

The San Francisco-based start-up has been mounting billion-dollar losses ahead of its market debut. Its adjusted losses totaled $1.85 billion in 2018, according to its initial IPO prospectus. Those losses slowed from 2017, when Uber lost $2.2 billion. The company increased its revenue to $11.3 billion, up 43 percent year over year.

Most tech companies are not known for making money ahead of public offerings. Lyft, which went public in April, had a loss of $911 million on $2.1 billion in revenue last year. Twitter was losing money when it listed on the New York Stock Exchange in 2013. Snap, Spotify and SurveyMonkey — which all listed in 2018 — were also bleeding money.

Lyft, Zoom and Pinterest all priced above their marketed range this year. The valuations for these tech unicorns are based on future profits, since almost none of their businesses are profitable yet.

Market valuation expert Aswath Damodaran has said the recent totals are far too high — or as he put it, "scary."

"I'm a little scared of Uber at $100 billion," the NYU Stern professor told CNBC. "I think both Lyft and Uber are struggling with a way to convert revenue growth into profits. So you are paying $100 billion for a company that still doesn't have a viable business model. That's scary."

Tesla Inc.’s first-quarter earnings and accompanying call with analysts was “one of (the) top debacles we have ever seen,” according to one longtime Tesla bull, who said Thursday he was dropping his buy rating on the stock.

Daniel Ives of Wedbush cut his rating on Tesla

TSLA, -3.72%

to neutral from outperform, the equivalent of buy, in a scorching note that reflected equal amounts of frustration and despair.

“In our 20 years of covering tech stocks on the Street we view this quarter as one of top debacles we have ever seen while Musk & Co. in an episode out of the Twilight Zone act as if demand and profitability will magically return to the Tesla story,” Ives wrote in a note to investors. “Ultimately we believe the company’s guidance is aggressive and management/board is not taking aggressive enough cost cutting actions and shutting down future endeavors to preserve capital and give a sustained path to profitability for the Street.”

Tesla late Wednesday posted a wider-than-expected first-quarter adjusted loss and missed revenue forecasts, although Wall Street appeared to zero in initially on promises that company executives made during their call with analysts, including that the car maker would be profitable again this year.

Tesla posted a loss of $702 million, or $4.10 a share, in the first quarter, compared with a GAAP loss of $4.19 a share in the year-ago period. Adjusted for one-time items, Tesla said it lost $494 million, or $2.90 a share, compared with a loss of $3.35 a share a year ago.

Revenue reached $4.5 billion, compared with $3.4 billion a year ago.

Analysts polled by FactSet had expected an adjusted loss of $1.15 a share on sales of $5.4 billion for the quarter. The per-share loss forecast had widened in recent days, and comes after Tesla reported third- and fourth-quarter GAAP and adjusted profits.

“In our 20 years of covering tech stocks on the Street we view this quarter as one of top debacles we have ever seen while Musk & Co. in an episode out of the Twilight Zone act as if demand and profitability will magically return to the Tesla story.”

The stock wavered between gains and losses in the extended session Wednesday, but took a dive Thursday of more than 4%.

JPMorgan analysts led by Ryan Brinkman said they expected a negative reaction, noting Tesla also missed margin and free cash flow estimates, while offering guidance that calls for another loss in the second quarter, against consensus expectations for a profit.

“Management also seemed less opposed to an equity capital raise, acknowledging ‘some merit’ to the idea, which in our view serves to highlight dilution risk that likely rises after 1Q cash flow and cash balance tracked weaker than JPM and consensus expectations,” Brinkman wrote in a note to clients.

JPMorgan rates the stock as underweight with a price target of $200 that is 20% below its current trading level. The company is forecasting deliveries to rise 43% to 59% in the second quarter versus the first, although even at that level, it expects to be loss-making, said the analyst.

“While 2Q deliveries guidance appears potentially aggressive, the full year outlook for 360-400K implies a further roughly +35% to +45% sequential increase from 1H19 to 2H19, further highlighting the execution risk entailed in meeting the figures that are implied needed to generate positive earnings and cash flow,” said Brinkman.

RBC analyst Joseph Spak said the numbers were “uglier than expected” and agreed a capital raise looks likely. Spak noted that spending on research and development was the lowest since the fourth quarter of 2016.

“Elon talked about putting Tesla on a ‘spartan diet’ and while we don’t doubt the company spent inefficiently in the past, the low capex+R&D and of course the lower sales, are not hallmarks of a hypergrowth company, yet TSLA continues to be valued as one,” he wrote in a note to clients, reiterating his underperform rating on the stock and $200 price target.

At Bernstein, analyst Toni Sacconaghi said the elephant in the room is still demand and questioned whether the report and call really offered any information.

“We can’t help feeling that Tesla sidestepped the issue on last night’s earnings call, with management resorting to prognostications rather than providing incremental data points,” he wrote in a note. “While we have long seen a plausible path to 400k Model 3 sales, our near-term visibility on demand / price elasticity remains limited.”

Bernstein rates the stock as market perform with a price target of $325.

Piper Jaffray took a more upbeat tone, reiterating its overweight rating on Tesla stock and guessing that the downside will be limited to the first quarter.

“Although logistical challenges—long with lower transaction prices—had an obvious impact on Q1 profitability, we think this was temporary,” analyst Alexander Potter wrote in a note. “Guidance implies a second-half recovery for both deliveries and margins, and this seems reasonable to us.

The first quarter “suffered from a particularly nasty combination of headwinds, including seasonality, a big buildup of non-US deliveries (negative for logistics costs and working capital), as well as the expiration of tax incentives in the United States,” said Potter.

Tesla made good on its pledge to improve affordability by cutting prices, thereby hurting margins. But that is a first-quarter issue that should not be repeated, he said. Piper is still with a stock price target of $396.

Analysts at Deutsche Bank said first quarter was a weak start of the year but results should improve in the coming quarters as Model 3 deliveries increase. The analysts, led by Emmanuel Rosner, did cut their price target on the stock by $10 to $280 and trimmed some estimates to account for weaker margins, they said.

Needham analysts, led by Rajvindra Gill, doubted management’s promise of a profit this year. Tesla has never generated an annual profit and it will face "deteriorating margins combined with decelerating revenue growth, pushing out profitability” further, they said.

Tesla shares have fallen about 25% in the year so far. The S&P 500

SPX, +0.09%

has gained 16% in 2019, while the Dow Jones Industrial Average

DJIA, -0.38%

has gained 9%.

Tesla Inc.’s first-quarter earnings and accompanying call with analysts was “one of (the) top debacles we have ever seen,” according to one longtime Tesla bull, who said Thursday he was dropping his buy rating on the stock.

Daniel Ives of Wedbush cut his rating on Tesla

TSLA, -3.34%

to neutral from outperform, the equivalent of buy, in a scorching note that reflected equal amounts of frustration and despair.

“In our 20 years of covering tech stocks on the Street we view this quarter as one of top debacles we have ever seen while Musk & Co. in an episode out of the Twilight Zone act as if demand and profitability will magically return to the Tesla story,” Ives wrote in a note to investors. “Ultimately we believe the company’s guidance is aggressive and management/board is not taking aggressive enough cost cutting actions and shutting down future endeavors to preserve capital and give a sustained path to profitability for the Street.”

Tesla late Wednesday posted a wider-than-expected first-quarter adjusted loss and missed revenue forecasts, although Wall Street appeared to zero in initially on promises that company executives made during their call with analysts, including that the car maker would be profitable again this year.

Tesla posted a loss of $702 million, or $4.10 a share, in the first quarter, compared with a GAAP loss of $4.19 a share in the year-ago period. Adjusted for one-time items, Tesla said it lost $494 million, or $2.90 a share, compared with a loss of $3.35 a share a year ago.

Revenue reached $4.5 billion, compared with $3.4 billion a year ago.

Analysts polled by FactSet had expected an adjusted loss of $1.15 a share on sales of $5.4 billion for the quarter. The per-share loss forecast had widened in recent days, and comes after Tesla reported third- and fourth-quarter GAAP and adjusted profits.

“In our 20 years of covering tech stocks on the Street we view this quarter as one of top debacles we have ever seen while Musk & Co. in an episode out of the Twilight Zone act as if demand and profitability will magically return to the Tesla story.”

The stock wavered between gains and losses in the extended session Wednesday, but took a dive Thursday of more than 4%.

JPMorgan analysts led by Ryan Brinkman said they expected a negative reaction, noting Tesla also missed margin and free cash flow estimates, while offering guidance that calls for another loss in the second quarter, against consensus expectations for a profit.

“Management also seemed less opposed to an equity capital raise, acknowledging ‘some merit’ to the idea, which in our view serves to highlight dilution risk that likely rises after 1Q cash flow and cash balance tracked weaker than JPM and consensus expectations,” Brinkman wrote in a note to clients.

JPMorgan rates the stock as underweight with a price target of $200 that is 20% below its current trading level. The company is forecasting deliveries to rise 43% to 59% in the second quarter versus the first, although even at that level, it expects to be loss-making, said the analyst.

“While 2Q deliveries guidance appears potentially aggressive, the full year outlook for 360-400K implies a further roughly +35% to +45% sequential increase from 1H19 to 2H19, further highlighting the execution risk entailed in meeting the figures that are implied needed to generate positive earnings and cash flow,” said Brinkman.

RBC analyst Joseph Spak said the numbers were “uglier than expected” and agreed a capital raise looks likely. Spak noted that spending on research and development was the lowest since the fourth quarter of 2016.

“Elon talked about putting Tesla on a ‘spartan diet’ and while we don’t doubt the company spent inefficiently in the past, the low capex+R&D and of course the lower sales, are not hallmarks of a hypergrowth company, yet TSLA continues to be valued as one,” he wrote in a note to clients, reiterating his underperform rating on the stock and $200 price target.

At Bernstein, analyst Toni Sacconaghi said the elephant in the room is still demand and questioned whether the report and call really offered any information.

“We can’t help feeling that Tesla sidestepped the issue on last night’s earnings call, with management resorting to prognostications rather than providing incremental data points,” he wrote in a note. “While we have long seen a plausible path to 400k Model 3 sales, our near-term visibility on demand / price elasticity remains limited.”

Bernstein rates the stock as market perform with a price target of $325.

Piper Jaffray took a more upbeat tone, reiterating its overweight rating on Tesla stock and guessing that the downside will be limited to the first quarter.

“Although logistical challenges—long with lower transaction prices—had an obvious impact on Q1 profitability, we think this was temporary,” analyst Alexander Potter wrote in a note. “Guidance implies a second-half recovery for both deliveries and margins, and this seems reasonable to us.

The first quarter “suffered from a particularly nasty combination of headwinds, including seasonality, a big buildup of non-US deliveries (negative for logistics costs and working capital), as well as the expiration of tax incentives in the United States,” said Potter.

Tesla made good on its pledge to improve affordability by cutting prices, thereby hurting margins. But that is a first-quarter issue that should not be repeated, he said. Piper is still with a stock price target of $396.

Analysts at Deutsche Bank said first quarter was a weak start of the year but results should improve in the coming quarters as Model 3 deliveries increase. The analysts, led by Emmanuel Rosner, did cut their price target on the stock by $10 to $280 and trimmed some estimates to account for weaker margins, they said.

Needham analysts, led by Rajvindra Gill, doubted management’s promise of a profit this year. Tesla has never generated an annual profit and it will face "deteriorating margins combined with decelerating revenue growth, pushing out profitability” further, they said.

Tesla shares have fallen about 25% in the year so far. The S&P 500

SPX, +0.06%

has gained 16% in 2019, while the Dow Jones Industrial Average

DJIA, -0.44%

has gained 9%.